Reserve Bank remains cautious over ‘domestic risks’

Board minutes reveal 'threat of inflation would stick around as long as productivity growth remained persistently weak'.

THE Reserve Bank is worried Australia’s economy could be weakened by a housing market slowdown accelerated by the federal budget, a readout of its last interest rates meeting shows.

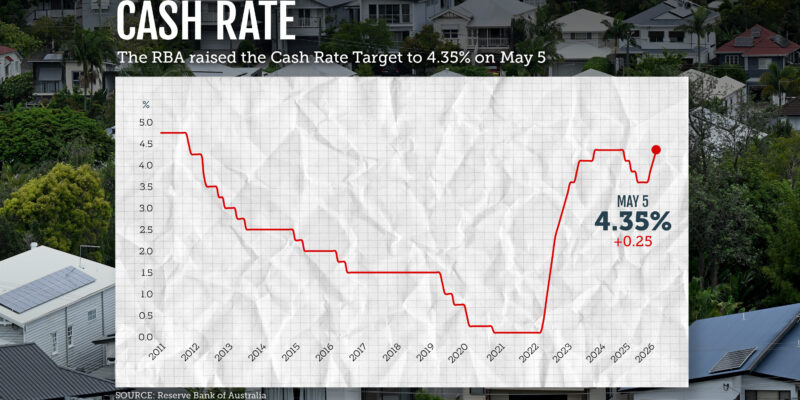

The central bank’s monetary policy board voted unanimously to hold the cash rate steady at 4.35 per cent at the May meeting, deciding that their previous three rate rises gave them enough space to assess how the Middle East conflict played out.

Hanging over the meeting was a tentative peace deal between the US and Iran, casting uncertainty over the future path for inflation and Australia’s economy.

If oil prices remained high, it could feed through to price and wage growth, entrenching inflation even if fuel prices eventually subside.

Even if the resolution held, it would take time to restore oil supplies to pre-conflict levels and demand would remain high as countries looked to replenish drawn-down inventories.

“These considerations led members to assess that the Middle East conflict still posed material upside risks for inflation and downside risks for growth,” according to the minutes, released on Tuesday.

But the board was also concerned about domestic risks.

The threat of inflation would stick around as long as productivity growth remained persistently weak, limiting the maximum rate the economy could grow at without pushing up prices.

On the other hand, the board noted the housing market had softened by more than expected, as a result of higher interest rates and tax changes for property investors announced in the Budget.

A material weakening in the housing market could inhibit growth in consumption, members noted.

That presented another impulse weighing on the economy.

The readout finished with the standard refrain that the board would “remain attentive to the data and the evolving assessment of the outlook and risks when making its decisions”.

But tacked on to the end was a hawkish phrase not present in the May minutes: the board would do whatever it considers necessary to achieve its mandate of low inflation and full employment, “including increasing the cash rate target if necessary”.

After softer-than-expected inflation data and falling oil prices, the RBA may not want traders to get too confident that the tightening cycle is over already.